(TXF) Delays and project cost overruns from the pandemic have meant lenders and sponsors of the Yunlin offshore wind farm in Taiwan are scrambling to remedy the project’s financial woes. ECAs may push out the tenor envelope to ease the pressure – but concrete solutions are yet to be realized.

The fledgling Taiwanese offshore wind market has struggled to take further flight against the economic headwinds left in the wake of the Covid-19 crisis. With China looking to cajole Taiwan into its fold, and pre-pandemic international bank appetite for such assets anemic without heavy cover, the financial foundations of this industry were built on export credit agency (ECA) support.

Over the past five years ECA-backed debt volumes to this nascent sector stands at $10.63 billion across eight deals, according to TXF Intelligence. ECA flexibility, alongside Taiwanese banks and insurers, was paramount to pushing the first batch of big-ticket projects – Yunlin, Formosa 2, CFXD, Changhua 1 – over the financial line. But ECA malleability will need to flex harder if the latest offshore wind project finance conundrum is to find concrete solutions.

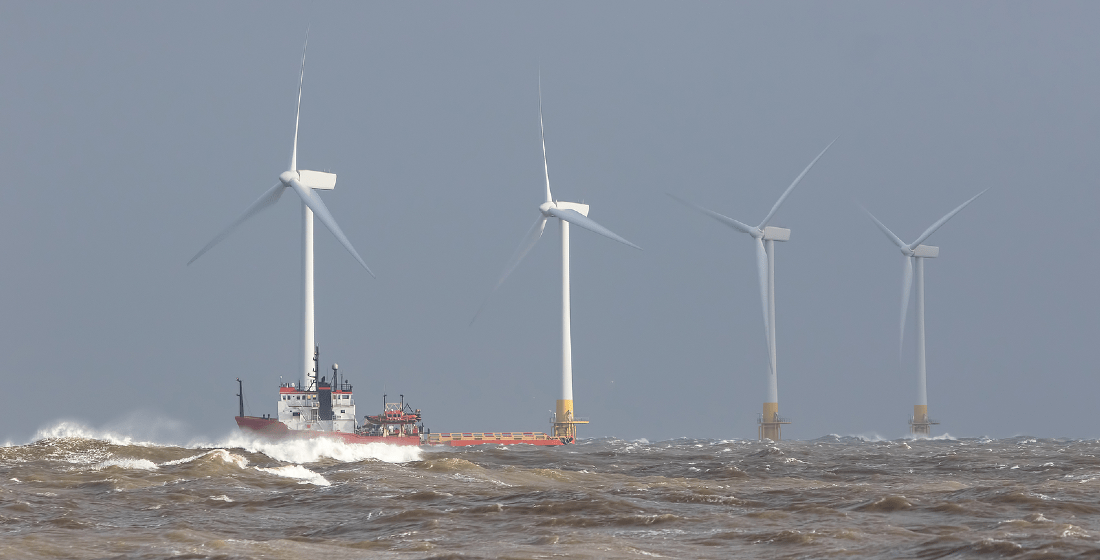

The NT$94 billion ($3 billion) 640MW Yunlin offshore wind scheme is in the doldrums, with doubled project costs causing sponsors to already put up three times the original equity commitments. The scheme, which was scheduled to reach commercial close in summer 2021, has been marred with technical issues and delays resulting from the pandemic.

And these points have been accentuated by the geography of the project in Taiwan – with April to September marking the only period for wind turbine installation. Due to this limited campaign period, any further delays would incur deeper setbacks for the project.

In short, Yunlin’s sponsors – Global Infrastructure Partner-backed Skyborn Renewables, previously the OSW business unit of German developer Wpd, is leading the consortium – need to start installing more wind turbines from April, when the climate conditions turn in favour of the project. The wind farm is currently 20% complete (with merely 16 out of 80 wind turbines installed so far).

Once the wind turbines commence operations and generate revenue, there will be a cash flow waterfall from the lenders to the sponsors. But in the meantime, there’s several viable solutions still on the table to rescue Yunlin, including a two-year extension to the tenor of the 18-year debt; an injection of fresh equity; an extension to the PPA by the government (unlikely) and waiving any penalties for the delays (more likely); and ECAs – Atradius, Euler Hermes, and EKF – pushing out the tenor envelope.

A tenor extension allows the sponsors to extend the repayment schedule, which grants the sponsors a higher equity internal rate of return and a more flexible debt service coverage ratio.

The other solution involves reopening the drawdown facility that currently has a drawstop in place. Discussions are also on with sponsors to inject more capital based on the availability of the revival of the drawdown facility.

The 19 original lenders have formed a working group and hired external consultants for the discussion, while the sponsors and the Taiwanese government began discussions to rescue the project in October 2022. ECAs are already undergoing survey and evaluation to explore options such as extending the tenor of their coverage. And there is also a potential haircut for lenders if the debt is restructured.

Despite ample liquidity, Taiwanese state banks are yet to shoulder construction risk for any of the ECA-backed offshore wind financings in recent years. And now, dogged government support may be even trickier for a private project ahead of the nation’s presidential election in 2024. So it seems the state banks’ risk aversion could pay dividends (for lack of a better expression).

In related news, JERA is planning to sell its 44% stake in the Formosa 3 project off the central-western coast of Taiwan according to a report by Nikkei. Perhaps the news comes as no surprise given the ongoing issues hampering Yunlin, with the Japanese utility concerned about high construction costs and low profitability.

The 2GW Formosa 3 is still in development and is expected to be launched in the second half of the decade, but deal gestation periods are lengthening in the Taiwanese offshore wind sector, not shortening, if project precedents are anything to go by.

JERA will retain an interest in the Formosa 1 wind power project, launched in 2019, and the nearby Formosa 2 project which is preparing to start operations after the last of its 47 wind turbine generators was installed last month.

Leave a comment