http://www.ft.com/cms/s/0/2d35d198-d6b7-11e4-97c3-00144feab7de.html#ixzz3VzBe4t6k

March 31, 2015 5:38 pm

Oil majors over a barrel due to falling reserves

Christopher Adams, Energy Editor/Financial Times

The world’s largest oil and gas groups shed more than a billion barrels of reserves in 2014, the sharpest decline in at least six years, according to figures that show their exploration record has worsened as big discoveries dwindle.

The latest annual reports for the ‘Big Five’ energy majors — BP, Chevron, ExxonMobil, Royal Dutch Shell and Total — show that proved reserves for the group as a whole shrank to 78.6bn barrels of oil equivalent last year, from a little over 80bn boe the previous year, the steepest drop since at least 2008.

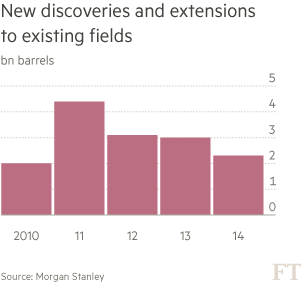

Behind the fall is a substantial decline in the number of barrels added as a result of recent discoveries and extensions to existing oil and gasfields, according to Morgan Stanley analysis of the data. That figure fell 24 per cent last year to 2.3bn boe and has nearly halved from 4.4bn boe in 2011.

Though these figures can be volatile, and depend in part on companies’ approach to booking barrels as “proved” reserves, the deteriorating exploration performance — if sustained — will raise questions over their ability to grow in the long run without making acquisitions.

Reserves are the bankable assets to which oil and gas companies must keep adding to maintain production in the future. They are required to publish data on proved reserves, which companies intend to develop, but not probable reserves.

Martijn Rats, analyst at Morgan Stanley, says that last year was “really quite disappointing” for discoveries made through exploratory drilling. Big finds, such as Statoil’s Johan Sverdrup field in the Norwegian North Sea in 2010, are increasingly rare.

“Discoveries are drying up,” he says. “It’s becoming harder and harder to find oil outside the US. There are great success stories in the US with shale gas and ‘tight’ oil, but, outside that, conventional drilling is becoming less and less successful.”

The annual reports are consistent with figures from IHS, the research company, which show discoveries of new oil and gas reserves dropped to their lowest level in at least two decades last year.

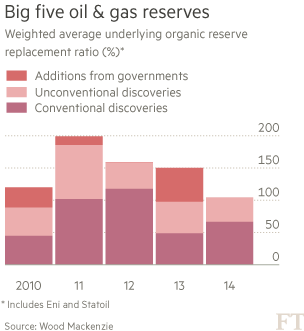

The five companies’ “organic” reserve replacement ratio, a measure of how much oil and gas is added to reserves relative to production, was 84 per cent last year, the lowest level since 2010. True, this ratio was dragged lower by sharp annual falls for Shell and BP. Only Chevron, though, reported a year-on-year increase in extensions and discoveries.

While the boom in US shale output has sent North America’s output soaring and contributed to the 50 per cent plunge in crude prices since last summer, the producers leading that resurgence in output have been smaller operators.

At the same time, under pressure from investors to improve returns following years of soaring cost inflation, the majors have curbed capital spending. Wood Mackenzie, the energy consultancy, predicts that industry-wide exploration budgets will be cut 30 per cent this year after the fall in oil prices.

A decline in reserves may be no bad thing if the quality of those reserves is improving. Indeed, dig deeper and the underlying picture is more complicated than year-on-year changes suggest. Though proved reserves fell for the ‘Big Five’ last year, the output life of those assets has been rising, up from 12.6 years in 2010 to 14.1 years in 2014.

In part, that reflects the nature of the barrels being added. Liquefied natural gas and Canadian oil sands, accounting for a substantial part of recently added reserves, have a longer life than conventional crude finds. This shift in assets should lead to more stable cash flows, say analysts.

Slower long-term reserves growth would be consistent, too, with a “value over volume” strategy that has become industry mantra against a backdrop of weaker oil demand. If the cost of developing reserves has soared and annual demand growth is predicted to slow to less than 1 per cent, why should companies continue to spend billions bulking up assets?

While the pace of discoveries has been disappointing, the high exploration and production spending of previous years have improved portfolio longevity, says Wood Mac’s Tom Ellacott.

The weighted average underlying organic reserve replacement ratio for a wider group, including Italy’s Eni and Norway’s Statoil, has fallen from 2011 levels of nearly 200 per cent to 104 per cent in 2014. But it has averaged a healthy 147 per cent for the past five years, Wood Mac estimates show.

“They are not heading for terminal decline,” says Mr Ellacott. “They have breathing space.”

Even so, unless the majors reverse the decline in discoveries — which looks unlikely as exploration is cut — they will need to find other ways to add to reserves.

One way to do this is to strike agreements with host governments that allow companies to book proven reserves, as Total and Shell have done with Brazil’s giant Libra field. Mexico’s auction of offshore stakes will be one such opportunity.

If a nuclear deal is reached with Iran that lifts western sanctions and opens the country to US and European investment, a shift to agreements that allow oil companies to book reserves might follow. Iraq, under severe budgetary pressure, has hinted it could switch from service contracts to production sharing deals.

Another way is through acquisitions. Mr Rats of Morgan Stanley says: “Historically the majors are not the most efficient explorers. Exploration tends to be done better by smaller companies. But where the majors really excel is in development.”

“When the oil price takes a sudden collapse, smaller companies get into trouble and their shares become cheap. The majors, with their very low borrowing costs, scoop up these assets at the bottom of the cycle. If executed well, it can be a very efficient way to add resources.”

And that is exactly what Exxon itself has hinted could happen, saying it is “alert” to bolt-on acquisitions. Analysts point to the US shale industry, where high indebtedness could make operators vulnerable, as a likely target. Having struggled to make it work in the past, the question for the majors now is whether they can afford not to be in shale. The answer may be no.

Copyright The Financial Times Limited 2015

Leave a comment