Up to a quarter of the active floating drilling rig fleet – drillship and semi-submersibles – could be scrapped, as the demand, which had never recovered from the previous downturn, is now expected to remain under pressure “until 2022,” Rystad Energy, a Norwegian energy intelligence firm said.

“The new downturn that the Covid-19 pandemic has brought upon the oil and gas industry has put many sectors in financial distress. Restructuring in the already-stretched offshore drilling market will accelerate, a Rystad Energy analysis shows, and the global floater fleet, whose utilization has been suffering since the previous downturn, can expect a new round of scrapping as a result,” Rystad said.

Rystad, which says that 154 floaters were scrapped since the last downturn, has evaluated active rigs in the global floater fleet and found that up to 59 of the 213 units are potential candidates for retirement.

“This equates to one-quarter of the floater segment, or 22 drillships and 37 semisubs,” Rystad, which says that drilling contractors need to cut rig supply to regain pricing power, says.

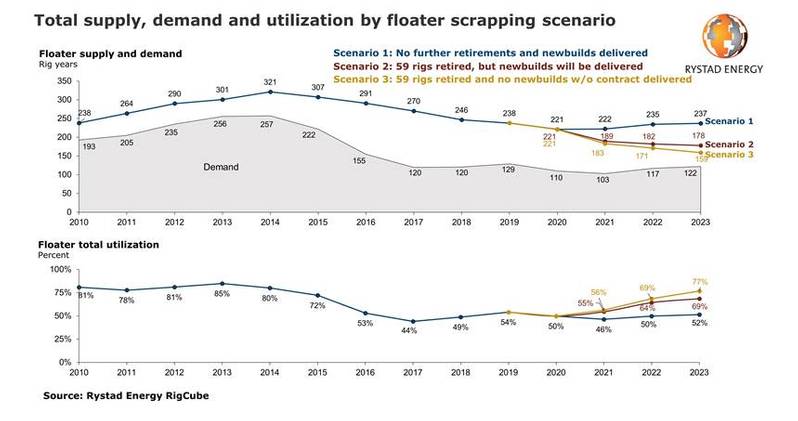

“Global demand for floaters had just started to recover before the pandemic and is now expected to remain under pressure until 2022. Demand is expected to fall from 129 rig years in 2019 to 110 rig years in 2020 and 103 rig years in 2021, before slowly inching back up to 117 rig years in 2022 and 122 rig years in 2023,” Rystad added.

Meanwhile, Rystad said, 25 newbuild floaters are planned for delivery towards 2023.

“Naturally, weak demand is going to keep utilization at low levels unless we see a meaningful increase in the price of oil,” it said.

Rystad Energy has created three scenarios, annualizing supply and demand in rig years, which show the range of the expected utilization levels based on rig attrition and newbuild deliveries. Utilization began plummeting in 2016 and has hovered between 45% and 55% since, with 2020 levels expected to stand at 50%.

Utilization began plummeting in 2016 and has hovered between 45% and 55% since, with 2020 levels expected to stand at 50%.

Utilization could reach 77% in 2023 if all 59 floaters identified by Rystad Energy are retired and no newbuild delivered – which, according to Rystad, is a rather optimistic scenario. Utilization will decline with each newbuild floater delivery, down to 69% if all these rigs make it out of the shipyard.

In Rystad’s last scenario, which assumes delivery of the newbuild units but not full retirement of the identified rigs, utilization could fall to as low as 52% depending on how many floaters are scrapped.

More M&A ahead?

“Capacity attrition can set the stage for a comeback in utilization and play a key role as the offshore drilling industry seeks to shore up its finances. After drillers come out of restructuring we could see more mergers and acquisitions, which again could result in more attrition,“ says Jo Friedmann, senior energy service analyst at Rystad Energy.

“A reduction in the number of drilling contractors through M&A will cut the number of bidders in any tender process. Rig supply needs to tighten for drilling contractors to regain pricing power,” Friedmann says, without going into details on who could buy whom in the offshore drilling space.

Per Rystad, many of the 154 floaters scrapped since the last downturn share common characteristics. Early in the cycle, the only units to be retired were semisubs, while rig owners now see the need to start retiring drillships, Rystad says.

“Most of the semisubs that were retired at the outset were the oldest, least capable units. Increased operator preference for high-specification drillships in benign markets also led to more scrapping in the benign semisub segment of the floater market,” Rystad added.

The Norweigan company says that floating rigs that were cold stacked relatively early on during the prior downturn will be some of the first rigs to be retired in this downturn.

“Rig owners have been waiting for a recovery that never really took off, and the number of units that have been cold stacked since 2016 are in the double digits,” Rystad says.

Further, according to Rystad, reactivation costs can range between $20 million and $35 million for rigs that have been warm stacked for a relatively short period of time to between $40 million and $100 million for rigs that have been cold stacked for longer periods of time.

“Given current rates and contract durations, most of these cold-stacked units are unlikely to return to work,” Rystad concludes.

Source: OE

Leave a comment