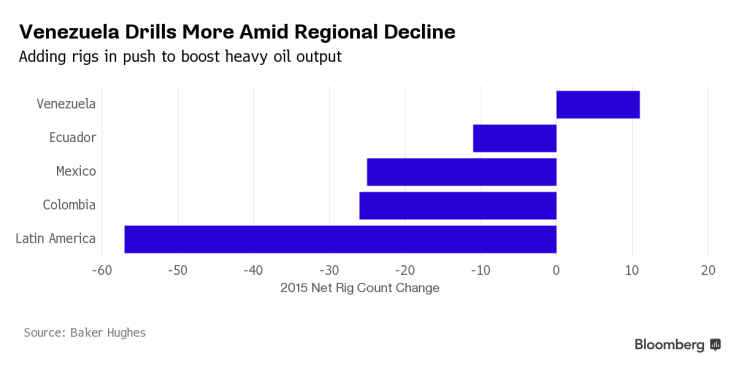

All across the Americas, drilling rigs are being idled as oil prices hover near six-year lows. In Colombia, more than 57 percent have been pulled; in Mexico, 42 percent.

Then there’s Venezuela. Starved for hard currency needed to ease a crushing recession and struggling to shore up slumping output, the state oil giant known as PDVSA has been adding rigs at a furious pace to search for new sources of crude.

The number has climbed 19 percent this year, signaling a new push that comes at the same time the OPEC nation is urging its fellow members to cut output at Friday’s meeting to support prices. It’s a sacrifice that Venezuelan President Nicolas Maduro — the successor to his mentor, the late Hugo Chavez — isn’t willing to take in his own country, though, as a shortage of dollars fuels widespread shortages and runaway inflation and puts the opposition on the verge of taking control of congress in elections this weekend.

Petroleos de Venezuela SA’s drilling efforts are helping boost production from the Orinoco heavy oil belt, according to Medley Global Advisors. That extra-heavy oil can be mixed with lighter domestic grades to maintain the nation’s exports and bring in much-needed U.S. dollars.

Leave a comment