Noble’s Rosetta Deal Is OPEC’s Problem

Deals and financing are putting off a shakeout in the U.S. oil sector

Work at a drilling rig in Texas is seen here. Noble Energy’s announced acquisition of Rosetta Resources does little to support oil prices in the near term. PHOTO: BRITTANY SOWACKE/BLOOMBERG NEWS

By LIAM DENNING/WSJ

May 11, 2015 1:56 p.m. ET

OPEC has apparently all but given up on oil prices getting back to triple digits and staying there over the next decade, in part because of the U.S. shale boom. Does Noble Energy’s $2.1 billion acquisition of Rosetta Resources offer the Organization of the Petroleum Exporting Countries a glimmer of hope?

It is possible the merger of these two shale drillers will ultimately aid a rebound in oil prices. For now, though, it demonstrates the exploration-and-production sector’s ability to keep going in adverse conditions.

Rosetta has capitulated, weighed down by rising leverage. Overstretched E&P companies are supposed to throw in the towel amid low oil prices. Besides companies just slipping into bankruptcy—as American Eagle Energy did last week—the pressure on cash flows leads struggling companies to sell out to bigger ones.

In theory, such consolidation ought to lead to more-efficient spending and some higher-cost prospects remaining undrilled. Therein, perhaps, lies some comfort for OPEC in the medium term.

For now, though, there isn’t much to be had. Besides Rosetta’s weakness, Noble’s all-stock offer is also facilitated by the bounce in its stock. Before Monday’s news, which sent it down by 6% by midafternoon, the stock was up almost one-fifth from its January low.

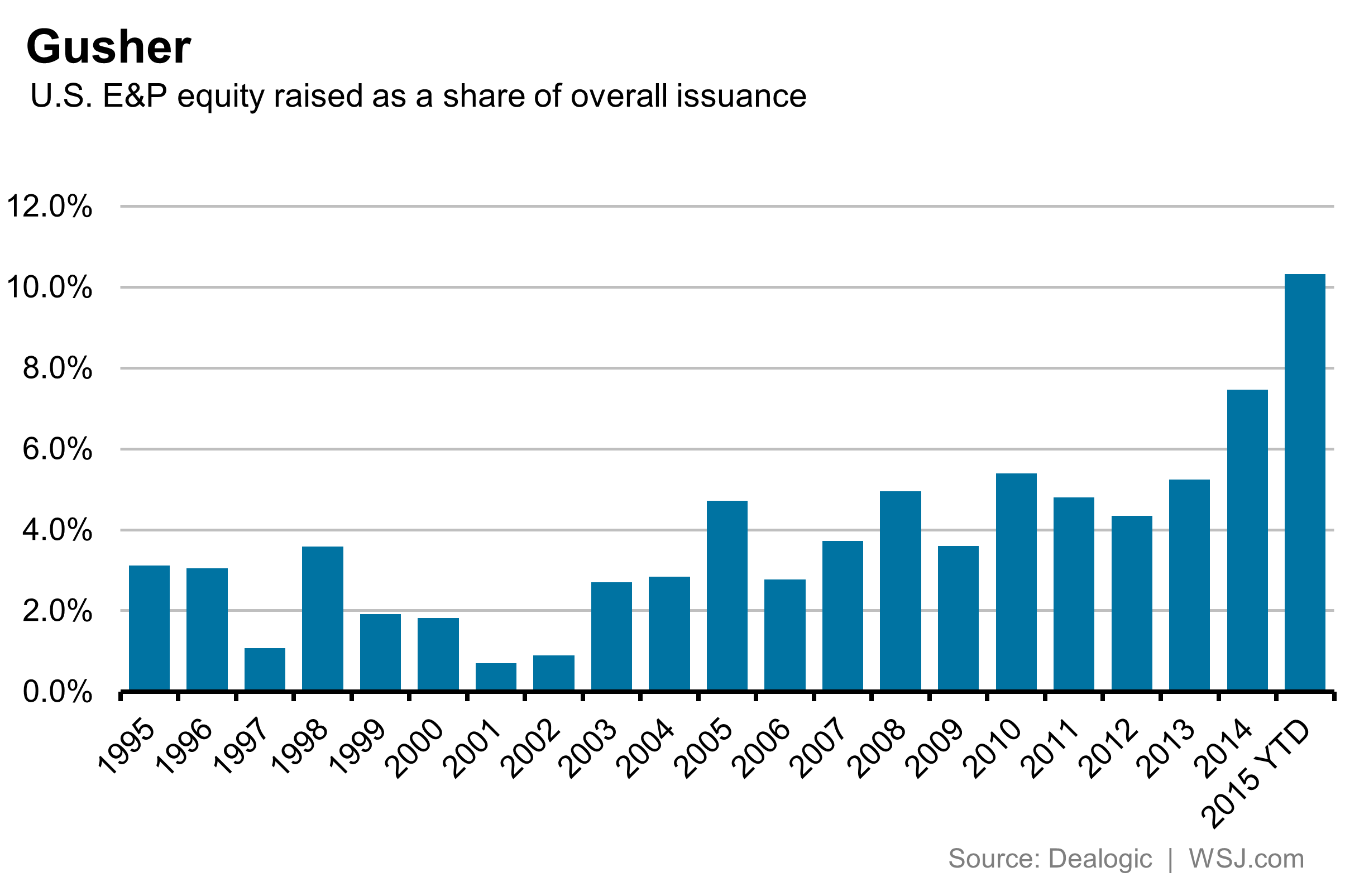

This fits a broader theme. E&P stocks on average bottomed out ahead of oil prices and the sector has taken advantage: So far this year, it has accounted for 10% of all equity raised in the U.S., the highest share since at least 1995, according to Dealogic.

Law firm Haynes and Boone found in a recent survey that roughly two-thirds of E&P borrowers are likely to see lending lines based off proven reserves cut in spring reviews. Yet Buddy Clark, a partner at the firm, sees E&P companies resorting to such things as second-lien loans provided by private equity as an alternative.

The upshot is that, despite the swift fall in oil prices and the U.S. rig count, signs of a slowdown in production are mixed so far. In a report this past weekend, Morgan Stanley said more than four-fifths of the E&P companies it covers either met or beat production forecasts in the first quarter, while a dozen raised full-year guidance.

America’s geology provides the foundation for the shale boom. But it is the country’s extraordinarily accommodating financial markets that have prevented it collapsing along with oil prices.

Leave a comment