Big Oil Companies Find Gains in Trading

Volatility, contango help BP and Shell during spell of low oil prices

The BP ETAP (Eastern Trough Area Project) oil platform in the North Sea. Amid the oil-price collapse, big oil companies are striking gains in their trading divisions. PHOTO: ANDY BUCHANAN/GETTY IMAGES

By

SARAH KENT/WSJ

May 6, 2015 11:54 a.m. ET

LONDON—Some of the world’s biggest energy companies are finding healthy profits amid the oil-price collapse in a little-publicized corner of their business empires: their trading divisions.

The world’s biggest oil companies came out better than many analysts had expected in the first quarter, cushioned somewhat by refining operations and cost-cutting despite a big drop in the price of oil from the same quarter a year earlier. But some of them, including BP PLC, Royal Dutch Shell PLC and Total SA, also got a lift from their trading divisions, vast operations focused on buying and selling oil and its financial derivatives.

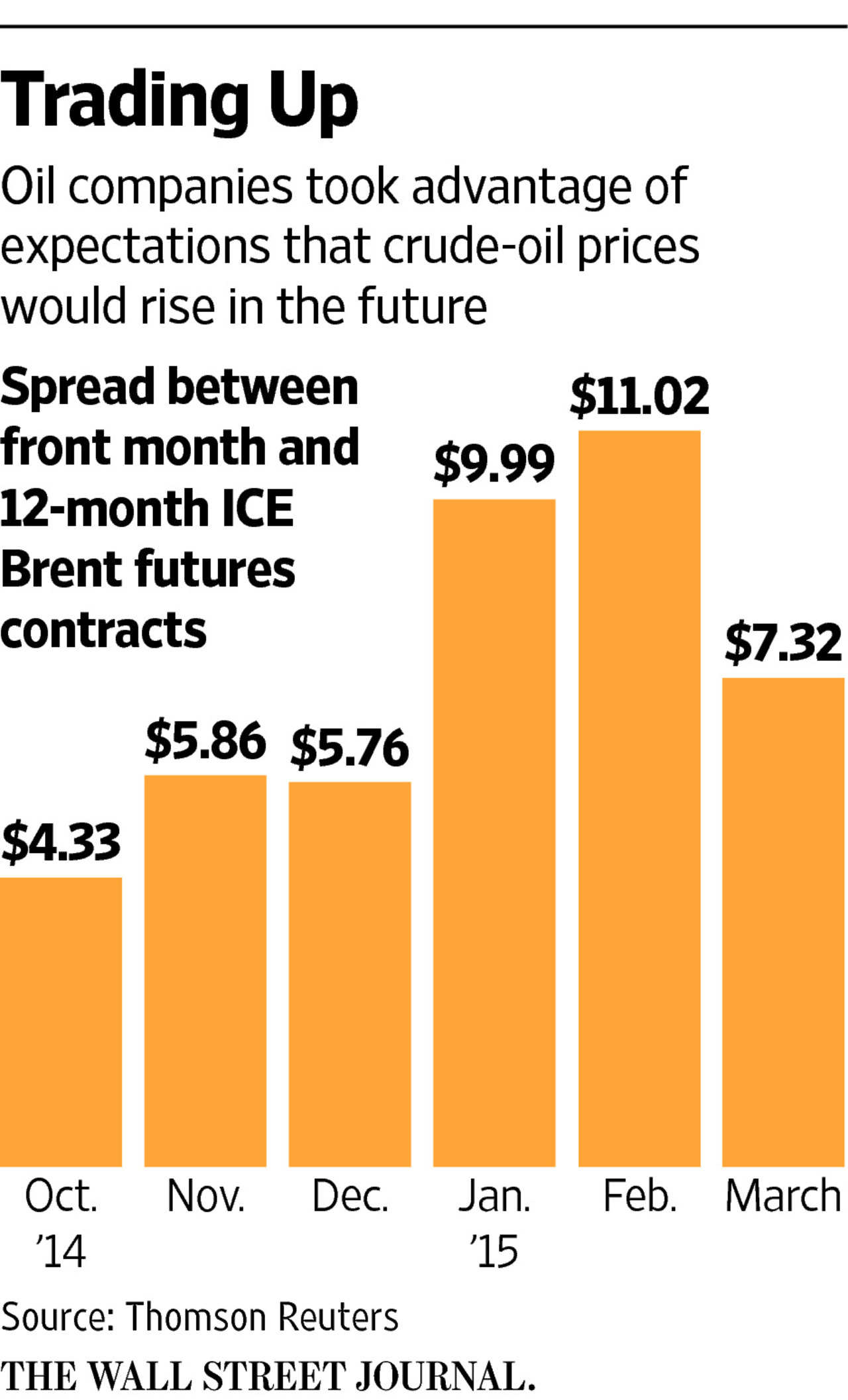

With Brent crude, the global benchmark, trading at roughly 40% of its 2014 peak, and even lower for much of the year’s first three months, traders were able to take advantage of large spreads between the current price of crude and the higher price of futures contracts.

It isn’t a subject the companies often talk about. None reveal their trading profits, and they say their trades are primarily done to get the most profit out of every drop of oil they produce.

Brian Gilvary, BP’s chief financial officer and former head of the U.K. oil company’s trading arm, declined to comment last week when asked to talk about the company’s trading profits beyond a disclosure that it had outperformed by $300 million to $400 million in the first quarter. Overall, the company’s net profit fell 40%.

“In terms of the oil-trading result, I mean, of course I can’t tell you,” Mr. Gilvary said during a call with analysts.

Shell was equally reticent. The company said oil trading helped cushion the blow of low prices, but it didn’t disclose how much. Its equivalent of net profit rose 7% in the first quarter.

Shell’s chief financial officer, Simon Henry,said the trading business was about “adding value” to its oil and natural-gas production.

“It’s not Wall Street trading à la Goldman Sachs,” Mr. Henry said during a media call last week.

It is an important distinction, as oil trading comes under greater scrutiny in Washington and Brussels. Because of their size in the derivatives market, units of Shell and BP are registered swaps dealers in the U.S. alongside banks and financial institutions as part of sweeping regulatory changes brought in under the Dodd Frank act in the wake of the financial crisis. The companies are also facing new trading regulations in Europe.

The most significant oil traders are based in Europe, with Shell, BP and Total leading the pack, backed by their substantial production volumes. U.S. oil companies such as Exxon Mobil Corp. and Chevron Corp. are also active selling the oil they produce, but haven’t developed their trading arms to the same extent.

When oil prices are low, or extremely volatile, trading divisions can really prove their worth, analysts say.

Before the oil market began its decline last summer, prices had been remarkably high and stable for years, limiting opportunities to trade on price disparities. With the oil market’s recent volatility, the chance to earn money with smart market moves has increased.

Trading companies such as the major oil companies with access to crude storage have also benefited in recent months from a market structure known as contango, which occurs when current prices are cheaper than those in the future. That allows companies to purchase oil now at the cheaper rates, store it and strike sales agreements at a higher price in the future, locking in profit.

“Our trading activities have generated strong results and we benefited from product market volatility and crude-oil contango structure,” said Patrick de la Chevardière,Total’s chief financial officer, during a conference call last week announcing quarterly earnings that were down 20% compared with a year earlier, but still better than expected by most analysts.

Most big oil companies consider trading part of their downstream sector, lumping it in with profits from refineries and retail gasoline stations. As the companies’ oil-extraction and exploration business, or upstream, takes a hit during a downturn, “the trading business is not necessarily affected and by that it provides a certain hedge against lower oil prices,” said Roland Rechtsteiner, global head of oil and gas at consultancy Oliver Wyman.

BP’s Mr. Gilvary said the company had $1.4 billion of working capital tied up in these kinds of storage plays in the first quarter and that those will unwind throughout the year. Shell’s traders have an “open credit line at the moment” to take advantage of the opportunities in the market, said Mr. Henry. Over the past six months they have used as much as $2 billion of that, he added.

Trading conditions could change as the oil price continues a slow recovery, breaking above $69 a barrel on Wednesday in London trading. The contango spread has also narrowed.

Conditions are still better than they have been in years though, profiting not just the major oil companies’’ trading arms, but also independent trading houses such as Trafigura Beheer BV and Glencore PLC. Remarkably high and stable crude prices squeezed oil trading margins in recent years. With the return of volatility, that has changed.

Write to Sarah Kent at sarah.kent@wsj.com

Leave a comment