Investors Grow Wary of Emerging-Market Debt

Fear of defaults grows as developing economies slow and dollar has climbed

As the U.S. Federal Reserve prepares to increase interest rates, the dollar has surged, raising concerns about the debt of some emerging-market companies that borrowed in dollars. PHOTO: ANDREW HARRER/BLOOMBERG NEWS

By CAROLYN CUI/WSJ

April 19, 2015 3:58 p.m. ET

Emerging-market bonds are being submerged in investors’ worries.

Facing rising corporate defaults from Brazil to China to Ukraine, some portfolio managers are selling debt issued by emerging-market companies.

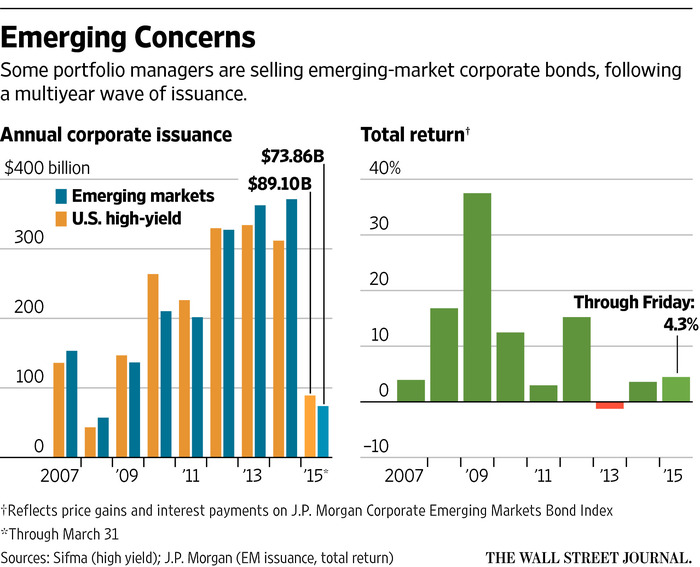

Since 2009, the market for emerging-market corporate bonds denominated in dollars and other hard currencies has more than doubled to $1.5 trillion, overtaking the amount of U.S. high-yield bonds outstanding. The gains were fueled by investors hungry for higher-yielding debt and willing to take on the extra risk of owning bonds of companies in developing markets.

Over that span, the market has delivered an annualized return of 11.1%, including interest and price moves, as measured by J.P. Morgan Chase’s Corporate Emerging Markets Bond Index.

But prices fell sharply late last year amid worries about companies’ ability to service the debt because of a surging dollar and slowing economies in the emerging world. Investors have flooded back to the U.S., looking toward an expected Federal Reserve interest-rate increase, the first since 2006, which is likely to put further upward pressure on the dollar.

Emerging-market debt prices have partly recovered recently, thanks to eased geopolitical tensions in Russia and stabilized oil prices. The J.P. Morgan emerging-market bond index has returned 4.3% this year as of Friday. Still, the prices of many such bonds remain lower than a year ago, and investors have been pulling money out of the sector.

Funds that invest in emerging-market corporate bonds have seen outflows for three consecutive months, a total of $556 million, according to EPFR Global.

“In countries where we’ll have a significant economic slowdown, an increase of defaults will put strains on the banking sector and potentially trigger a macro event,” said Bryan Carter, an emerging-market debt manager at Acadian Asset Management, which oversees $70 billion in assets.

As the Fed prepares to raise interest rates, emerging-market companies that have borrowed overseas are susceptible to swings of foreign capital that can make it harder for them to refinance debt. A rising dollar also increases the cost of paying off their dollar-denominated bonds.

Among companies in emerging markets, nonfinancial-sector debt in 2014 hit a record 83% the gross domestic product of these countries, according to the Institute of International Finance, a trade group for financial institutions. In comparison, the overall indebtedness at the government level has stayed flat in recent years, as emerging-market governments have been carefully managing their external debt.

“What’s at risk is not the country.…It’s the credit risk of the corporates,” said Jan Loeys,chief investment strategist for J.P. Morgan.

In Brazil, companies are paying an average across a range of bond maturities of 6.81% to borrow, up from 5.98% a year earlier, according to J.P. Morgan, while yields on Ukrainian bonds are at 29% on average, up from 14% a year earlier. As bond prices drop, yields rise.

It’s “a challenging mix” for emerging-market corporate bonds, said Dan Senecal,managing director at Newfleet Asset Management, which has $13 billion in assets under management.

Emerging-market corporate issuers were hit with 132 credit-rating downgrades in the first quarter, compared with just 25 upgrades, according to J.P. Morgan. That is the largest net-downgrade figure in at least five years.

Several recent high-profile corporate defaults have further raised investors’ concerns. In January, China’s Kaisa Group Holdings Ltd. became the first Chinese property developer to default on bonds sold outside China, heightening market fears about the real-estate sector.

Newfleet sold its Kaisa bonds at a loss rather than holding them during a restructuring, Mr. Senecal said. The reversal prompted the firm to sell its Chinese property-sector bond holdings while reducing its emerging-market high-yield corporate exposure.

Also this year, OAS SA of Brazil defaulted on its debt as Petróleo Brasileiro SA, the oil giant engulfed in a corruption investigation, stopped paying subcontractors. In Ukraine, a severe shortage of foreign reserves has hampered efforts by companies to repay external debt.

J.P. Morgan expects the default rate among emerging-market high-yield corporate issuers to reach 5.4% this year, up from 3.2% in 2014. In comparison, less than 2% of U.S. junk bonds are expected to default this year, according to Fitch Ratings Inc.

Managers of the $10.2 billion TCW Emerging Markets Fixed Income Total Return Strategy also reduced their exposure to high-yield corporate bonds late last year, particularly those issued by oil producers and explorers, said portfolio manager Dave Robbins. The fund increased its holdings of sovereign debt.

Other investors argue that the impact of a surging dollar will be limited. Adrian Petreanu,a portfolio manager at Ashmore Group, which has $61 billion under management, said many emerging-market debt issuers are exporters that will benefit from depreciating currencies.

Their costs are falling while their dollar-denominated export revenues provide a natural hedge against a rising greenback, he said. But companies that have borrowed in dollars and have no revenue in the same currency “will be in trouble,” Mr. Petreanu said.

Others say selecting the right issuer is the key. It is important to keep macroeconomic risks in mind so as to “avoid being in countries which will drag even excellent companies into default,” said Brigitte Posch, who heads the emerging-market corporate-debt strategy at Babson Capital, which has $217 billion in assets under management.

One in five emerging-market corporate issuers is a first-time issuer and nearly half of the existing issuers have only one bond outstanding, according to J.P. Morgan.

“The list of names that we would not invest in has grown,” said Mr. Carter of Acadian Asset Management.

Write to Carolyn Cui at carolyn.cui@wsj.com

Leave a comment