Halliburton’s Dimming Expectations

Although the Halliburton-Baker Hughes deal looks different months later, it still makes sense.

Baker Hughes, which Halliburton is buying, recently said it would stop publishing its closely watched North American well-count report in a cost-cutting measure.

Baker Hughes, which Halliburton is buying, recently said it would stop publishing its closely watched North American well-count report in a cost-cutting measure. PHOTO: AARON M. SPRECHER/BLOOMBERG NEWS

By SPENCER JAKAB

April 19, 2015 12:31 p.m. ET

It is hard to say if Halliburton Co. should be pleased with or spooked by the news.

While it is nice to hear that the company it is in the process of buying—No. 3 oil-field-services provider Baker Hughes Inc.—is watching the bottom line, its latest cost-cutting is chilling. To save money, Baker Hughes will even stop publishing its closely watched North American well-count report.

That is akin to shutting off the scoreboard in the late innings of a baseball game to conserve electricity—not that it is pleasant viewing for the Houston team these days. There are fewer wells to count amid an industry rout.

As much as Halliburton might like to save money, too, by getting rid of quarterly reports, that isn’t an option. And Monday’s first-quarter results won’t make for pleasant reading: Earnings per share are seen dropping to 41 cents versus 73 cents in the same period a year earlier.

PHOTO: THE WALL STREET JOURNAL

Back in mid-November when Halliburton agreed to buy Baker Hughes for $35 billion, it seemed like a deft move. Valuations had dropped following a big fall in crude prices. Then they kept on tanking, along with an even sharper decline in expectations for service-sector profits.

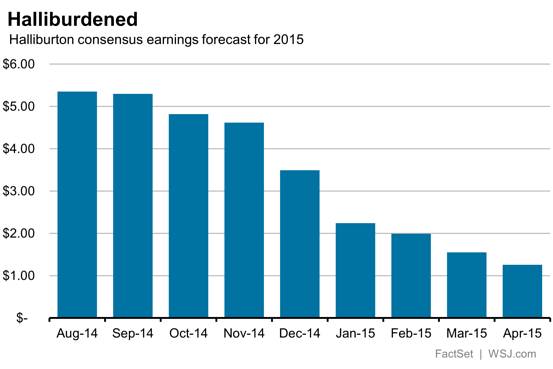

For example, in August 2014, analysts saw Halliburton earning $5.35 a share for 2015. By the beginning of November that forecast had fallen to $4.62. Today, it is even lower at $1.26.

A similar pattern is evident at Baker Hughes. The forecast for its cumulative net income between 2015 and 2017 has dropped by $3.7 billion from what was projected in late October. The difference is equal to more than 10% of the deal’s original value.

That is unfortunate, although the deal’s structure lessens the sting. Of the nearly $79-a-share offer price, just $19 is in cash; the remainder is in shares. And the companies project some $2 billion in annual cost savings.

Investors seem to have priced in some lean years and may yet be pleasantly surprised by the merger’s benefits. The combined value of the two companies today, plus net debt, equals about 1.8 times their projected revenue over the next 12 months—around what they fetched in the fall of 2009. That means the deal could end up looking better in hindsight.

Houston, we have a solution.

Leave a comment