Teetering on Junk, Petrobras Intrigues High-Yield Investors

Massive debt of troubled Brazil-owned energy firm could rally as a fallen angel

Brazil’s state-run energy firm, known as Petrobras, had its bonds downgraded into junk territory by Moody’s. If Fitch or S&P follows suit, Petrobras’ status as a fallen angel may make it a worthy risk for investors due to its high yield. PHOTO: VANDERLEI ALMEIDA/AGENCE FRANCE-PRESSE/GETTY IMAGES

By

CAROLYN CUI/WSJ

Updated April 3, 2015 6:06 a.m. ET

Petróleo Brasileiro SA, Brazil’s biggest company by revenue, has lost its investment-grade bond rating from Moody’s Investors Service and is in danger of being downgraded by other rating firms as it grapples with the financial fallout from a corruption scandal.

For some bond investors, now is the time to start buying.

That is because companies that tumble into junk-bond territory—called fallen angels—frequently see their debt rally in the wake of the downgrade as investors seeking high-yield securities swoop in to buy.

If either Standard & Poor’s or Fitch Ratings Inc. follows Moody’s, the company will be considered a full-fledged fallen angel. S&P decided March 23 to maintain its investment-grade rating. Fitch rates Petrobras, as the state-owned energy company is known, at one notch above junk.

Petrobras has about $56 billion in bonds outstanding and would be the largest fallen angel since at least 2005, according to data from J.P. Morgan Chase & Co.

Eric Fine, a portfolio manager of Van Eck Global’s $243 million Unconstrained Emerging Markets Bond Fund, said he began buying the company’s bonds “as they started to trade at prices that already reflected a downgrade.”

As of Feb. 28, Van Eck’s fund had about 4% of its assets in Petrobras bonds, according to its filings.

A second Petrobras downgrade also would force fund managers limited to investment-grade debt to sell, prompting a reshuffling of a J.P. Morgan index that tracks emerging-market corporate junk bonds.

Petrobras would account for almost 12% of the benchmark, requiring a small group of managers who track it to sell existing holdings to make room for Petrobras bonds.

“It’ll be such a big issuer in the high-yield index, which will create inefficiency and distortions in the markets,” said Samy Muaddi,a portfolio manager for T. Rowe Price Group Inc.’s emerging-market corporate bond strategies. The firm holds less in Petrobras bonds than the benchmark indicates.

Most emerging-market bond managers follow a broader J.P. Morgan emerging-markets index that includes high-yield and investment-grade companies. Less than $100 billion of funds is allocated based on that index, the bank says.

Another downgrade looms as Petrobras tries to sort out the impact of a corruption investigation that led to the resignation of Chief Executive Maria das Graças Silva Foster,Chief Financial Officer Guilherme Barbassa, and four other top executives. The massive scandal, which has ensnared high-ranking politicians and numerous Brazilian companies, is threatening to cut into the country’s growth this year.

The company, which hasn’t released audited financial statements since August, has been frozen out of the capital markets, forcing it to cut production and slow expansion as it struggles to generate cash.

A fallen angel isn’t necessarily a pariah.

When General Motors Co. was cut to junk in 2005, its bonds rallied for months. This year, Russia’s sovereign bonds were among the top performers, despite the country’s loss of its investment-grade rating.

Prices of Petrobras bonds already have dropped precipitously as its credit profile worsened and jittery investors fled. The difference in yields between its bonds and Treasurys, considered risk-free because of the U.S. government’s backing, have widened to levels only seen among junk bonds.

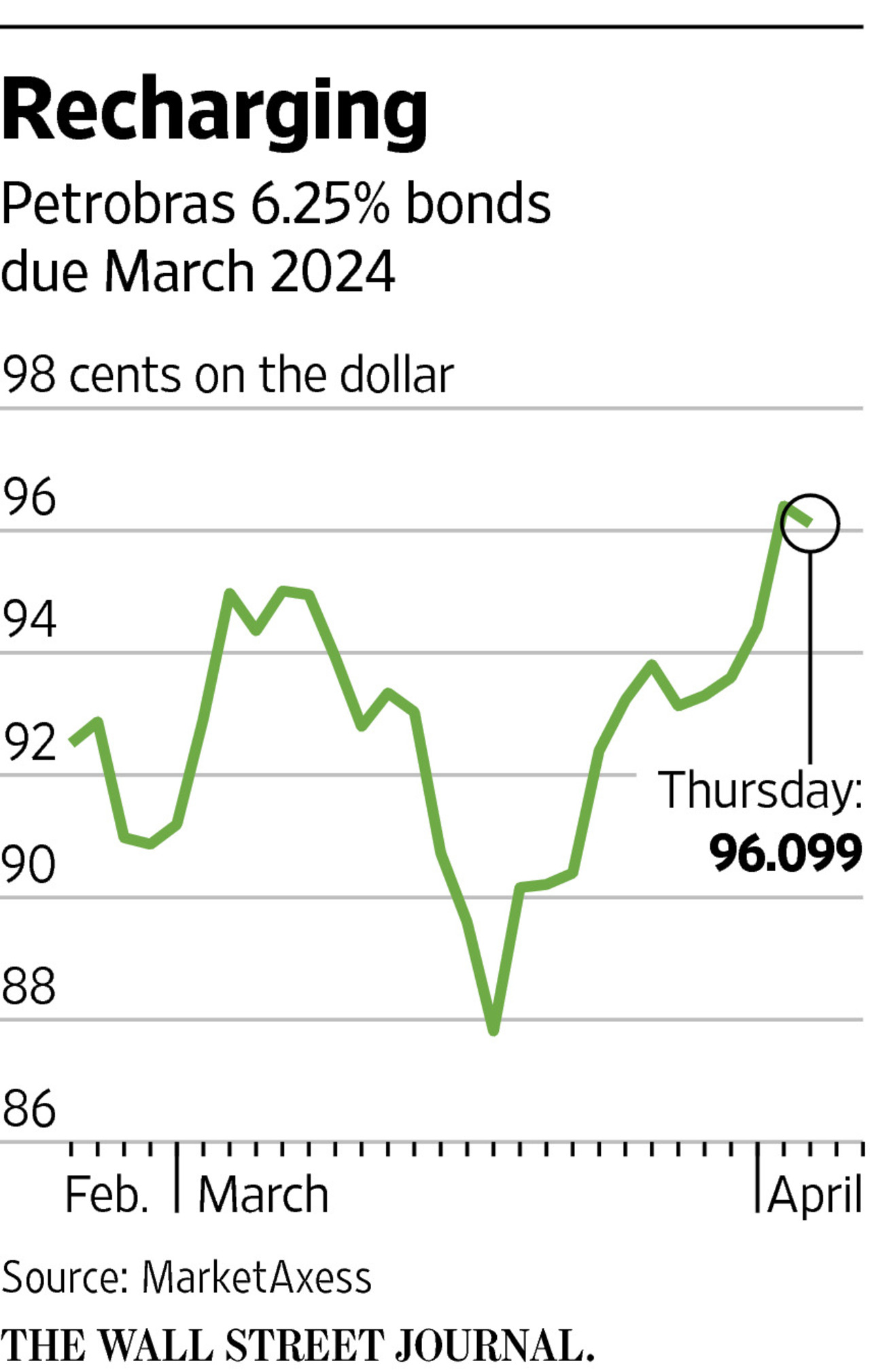

But the bonds have shown some signs of life lately. Petrobras bonds maturing in March 2024 have risen 4% in price since Moody’s downgrade in late February to 96.1 cents per dollar, according to MarketAxess.

Some investors are betting that the Brazilian government will help the company if needed. Petrobras has until the end of April to release its audited results.A failure to do so could trigger a technical default on its bonds, and creditors will have the right to request full repayment after a certain period.

In its decision to hold off downgrading Petrobras, S&P’s analysts cited “very high likelihood of extraordinary government support under a distressed scenario.” As a standalone company, the rating firm said, Petrobras’ credit rating would be junk.

On Wednesday, the China Development Bank threw a lifeline to Petrobras with a $3.5 billion financing deal. But investors are skeptical that such fixes would be enough to fill the company’s growing funding gap over the next few years.

At HSBC Global Asset Management, managers picked up some Petrobras bonds between November and January, after staying away from them for about a year, said Guillermo Osses, head of its emerging-market debt portfolio.

The fate of Petrobras is intertwined with its home country, Mr. Osses said. HSBC manages $149 billion in emerging-market assets.

“We like the credit,” said Jack Deino, head of emerging-market fixed-income portfolio management at Invesco Ltd., which has about $809 billion in assets under management. A lot of investors who are concerned about the ratings have already gotten out of Petrobras, and the current yields are attractive to high-yield investors.

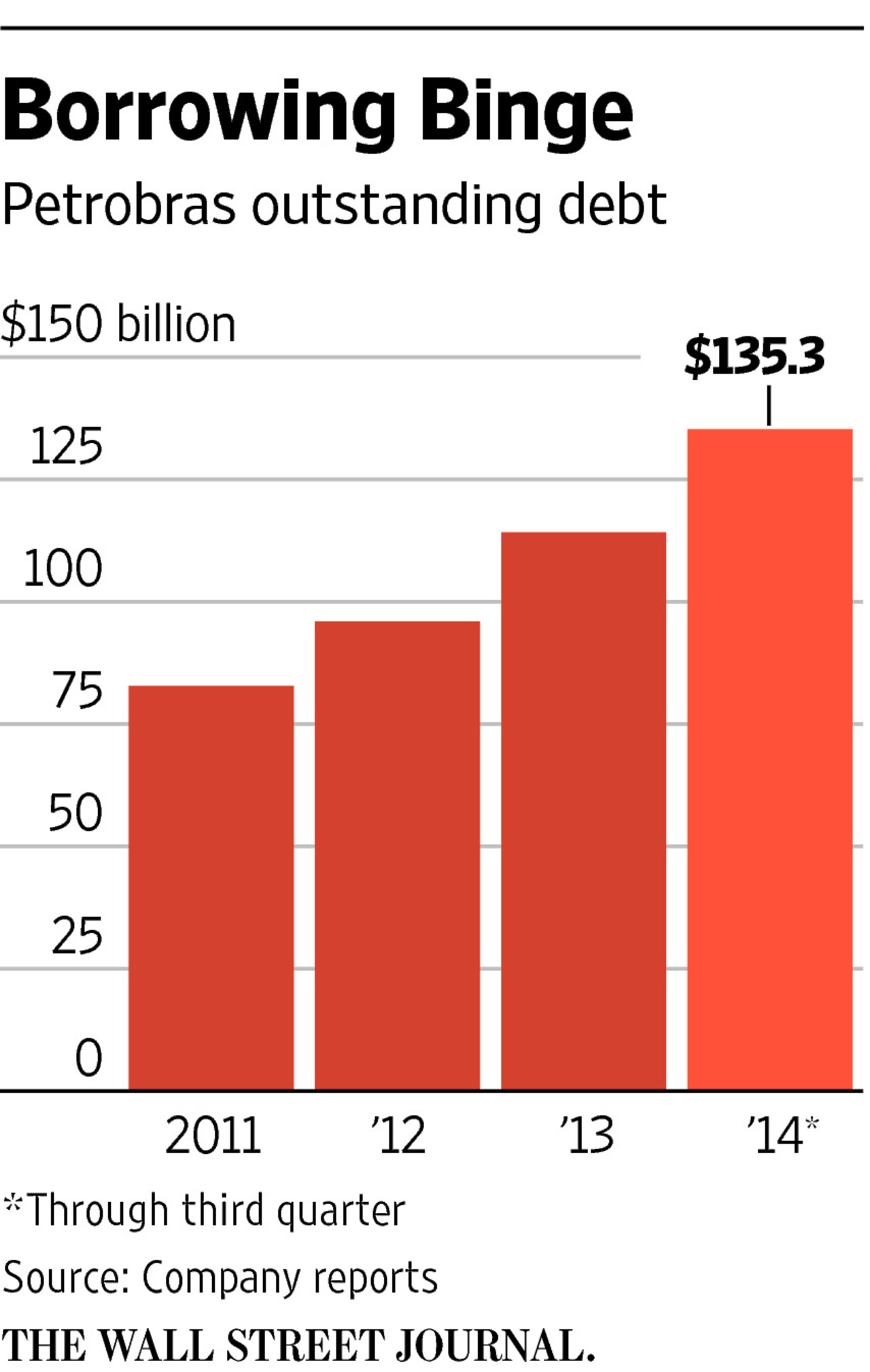

Petrobras in recent years seized on the investor appetite for emerging-market debt and went on a borrowing binge. Since 2011, the company has increased its debt load by 63% to $135 billion through the third quarter last year. About 60% of its debt is in dollars, according toNymia Almeida, Moody’s lead analyst for Petrobras. With the foreign financing, the company was able to ramp up production and discovered some rich oil reserves.

But fate has turned against it recently. A slowdown in China, which has been a major importer of Brazilian commodities, and a looming increase in U.S. interest rates have hit the country’s economy. Brazil’s currency, the real, has weakened significantly as the country’s balance of payments worsens. This puts Petrobras in a precarious position: the amount of debt it owes to itscreditors grows every day the real depreciates against the dollar.

Some managers are keeping their distance.

Jack Flaherty, a portfolio manager of the GAM Unconstrained Bond Strategy, said the fund hasn’t held Petrobras bonds “in any real way” for a long time. “For me, I still see a lot of risk in this story,” he said. GAM has over $124 billion in assets under management.

But given the sheer size of Petrobras bonds, emerging-market managers say they can’t overlook the company.

“I watch it every day, thinking about and trying to get my arms around it,” Mr. Flaherty said. “It could be an opportunity at some point but we’re cautious now.”

Write to Carolyn Cui at carolyn.cui@wsj.com

Leave a comment