Petrobras: Still Working at the Car Wash

The Brazilian oil major’s mammoth write off doesn’t address bigger challenges around its debt burden.

A Petrobras refinery. The company’s delayed 2014 results included nearly $17 billion in write-downs. PHOTO: NELSON ALMEIDA/AGENCE FRANCE-PRESSE/GETTY IMAGES

By

LIAM DENNING/WSJ

April 23, 2015 1:50 p.m. ET

Petrobras is emerging from its car wash looking more smashed up than shiny.

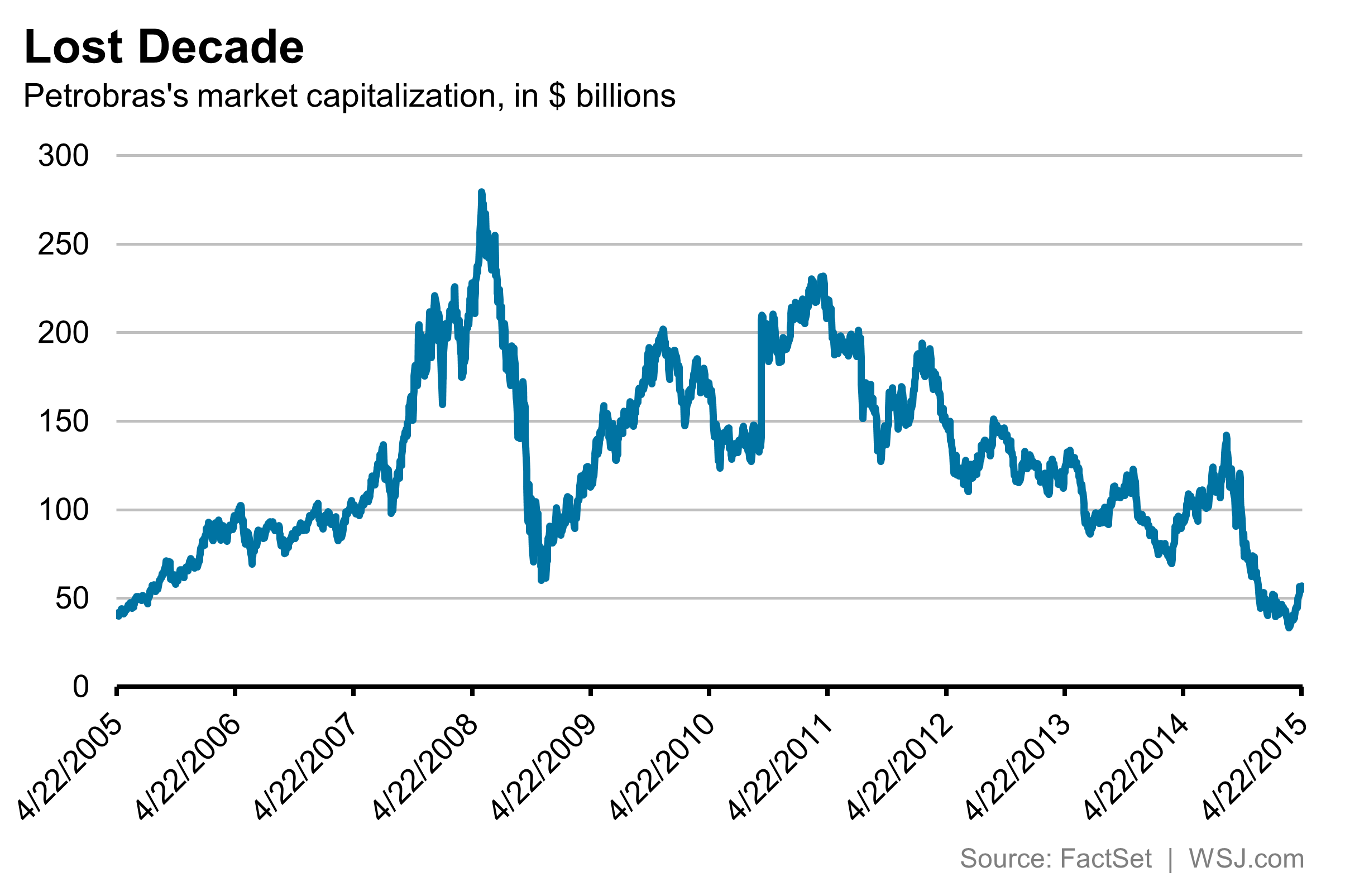

“Operation Car Wash” is the investigation into alleged corruption at Brazil’s state-controlled oil company. Petróleo Brasileiro on Thursday hosted a call to discuss its delayed 2014 results that included almost $17 billion of write-downs. Equivalent to almost one-third of Petrobras’s battered market capitalization, these are clearly intended to draw a line under the scandal.

The problem is that the company’s challenges are much bigger than just that. Exhibit A: net debt. This was $106.2 billion at the end of 2014, equivalent to almost 4.8 times last year’s earnings before interest, taxes, depreciation and amortization. By comparison,PetroChina is at about 1.4 times. So Petrobras is an oil major with the leverage of a Texas wildcatter.

It ran up that debt partly by spending to develop Brazil’s huge offshore “presalt” oil fields. These projects break even at a Brent crude price of around $50 to $55 a barrel, Itaú BBA estimates. That is still competitive with futures now averaging about $70 over the next three years. But the rewards are much lower than when triple-digit oil prevailed.

Another drain on cash has stemmed from Petrobras having to absorb losses arising from buying oil at market prices but selling refined products at regulated prices in Brazil. J.P. Morgan Chase estimates this cost Petrobras about $40 billion over the past four years.

Petrobras is slashing spending, as well as suspending its dividend. That is necessary. For investors, though, what once was a growth story is now a deleveraging play—and an uncertain one at that.

Besides volatile oil prices, Petrobras is highly sensitive to movements in the Brazilian currency, down 23% against the dollar in the past year. A weakening real suppresses critical refining margins and adds to the debt burden, two thirds of which is denominated in dollars. Deustche Bank forecasts that adverse currency moves—along with such unknowns as disposal proceeds in a weak oil market, heavy fines, or production problems—could push leverage above six times Ebitda next year.

While Petrobras’s new management insisted on Thursday that there are no plans for a dilutive share sale to fix the balance sheet, it can’t be ruled out.

It is tempting to think a company whose market value has dropped by about 75% in the past four years can’t go any lower. But, with a nod to Petrobras’s legal woes, investors should recall the opening line of disco classic “Car Wash”: “You might not ever get rich.”

Leave a comment